The Structural Case for a Canadian Airport Corporation

Canada captures neither the operating revenue nor the equity returns from its airports. Four decades of international precedent show what the alternative looks like.

On April 28, 2026, the Spring Economic Update committed the Government of Canada to assess alternative ownership models for the country’s twenty-one National Airports System airports. That assessment is now live in Cabinet. The question on the table is which structure to choose.

The diagnostic that organizes that choice is the one every country before Canada has had to answer: what is an airport for? An asset to sell, or a tool to build a national operator. The answer determines which revenue streams accrue to the country and which do not.

Two revenue streams flow from airport infrastructure. The first is operating revenue — aeronautical fees, retail and food-and-beverage, parking, real estate, and the broader commercial program. The second is equity returns — dividends and capital appreciation on the operating entity. Whoever operates the airport captures the first. Whoever owns the equity captures the second. The two streams are independent. A country can capture both, one, or neither, depending on how it structures ownership.

Canada today captures neither at scale. The 1992 airport authority structure made the operators non-profit and issued no equity. Operating margins are retained at each airport and reinvested locally. There is no national operator to consolidate them. There is no equity to dividend or appreciate. The Maple 8 pension funds — together managing approximately $2 trillion — have for two decades captured both streams as foreign investors at airports across Europe, Asia, the Pacific, and the Americas. At home, the same structure makes Canadian equity ownership of Canadian airports impossible. Aviation Deep has previously documented that Canadian airport authority aeronautical fees, despite the non-profit status of the operators, run higher than the fees at airports PSP operates abroad. The 1992 structure is not delivering lower costs to users.

Four decades of international precedent show how the alternatives have actually performed.

Spain consolidated forty-six airports under AENA in 1991, corporatized in 2010, and listed 49 percent on the Madrid Stock Exchange in 2015 while retaining 51 percent through Enaire. Between 2015 and 2023, AENA paid the Spanish state €4.857 billion in dividends, and the share price has appreciated 270 percent since the IPO. The international segment, which generated nothing in 2015, generated €913.7 million in 2025 through stakes in Brazil, Mexico, Colombia, Jamaica, and the United Kingdom. Spain captures both streams.

France took the same path on a different timeline. Aéroports de Paris listed in 2006 with the French state retaining majority control. ADP today operates or holds stakes in airports across the Middle East, Latin America, Central Asia, and India, and acquired TAV Havalimanları in 2017 — placing TAV’s portfolio across Turkey, the Balkans, the Caucasus, and the Middle East under French ownership. France captures both streams.

Germany lists Fraport on the Frankfurt Stock Exchange with a state-aligned majority composed of the State of Hesse, Stadtwerke Frankfurt, and Lufthansa. Fraport operates Lima, Antalya, Burgas, Varna, Sofia, Pulkovo, and additional airports in Asia and Europe. Germany captures both streams.

Brazil chose a different structure. Multiple concession rounds since 2011 have transferred operations of dozens of airports to private operators under thirty-year concession contracts. The model has delivered capital investment and operational professionalization. It has not produced a Brazilian national operator. The state captures one revenue stream — the concession fee — and bears construction and demand risk through guarantees. The dual capture is not available.

The United Kingdom sold BAA in 1987. After the 2009 Competition Commission breakup, the UK airport system is today held by a consortium of sovereign wealth funds, infrastructure funds, and pension funds. The United Kingdom captures neither revenue stream from its flagship airport. Among the foreign owners of UK airports is PSP Investments — Canada’s federal public sector pension fund — which holds Aberdeen, Glasgow, and Southampton through its AviAlliance subsidiary. PSP captures both operating revenue and equity returns from those airports, as a foreign investor. The Canadian state captures nothing from its own airports. The asymmetry is documented, not hypothetical.

Australia chose a third path. Between 1997 and 2002, the federal government leased its major airports — Sydney, Melbourne, Brisbane, Perth, Adelaide, and others — to private consortia under fifty-year arrangements. Australian superannuation funds, principally IFM Investors, AustralianSuper, UniSuper, and the Future Fund, acquired the operating equity. The Australian Competition and Consumer Commission monitors aeronautical pricing and service quality. Operating revenue and equity returns are captured by Australian institutional investors, not by foreign capital. The federal government captures neither stream on an ongoing basis — only the original lease consideration. Australia retained domestic capital ownership without building an Australian national operator with international platform reach.

Five conditions distinguish Canada from any of these precedent countries at their decision point.

The Maple 8 sits on approximately $2 trillion in committed capital with stated infrastructure allocations.

Twenty years of Canadian operating expertise sits inside PSP’s AviAlliance platform — Athens, Düsseldorf, Hamburg, San Juan, Aberdeen, Glasgow, Southampton — and Vantage, the operator launched out of Vancouver International.

No fiscal forcing function is driving the timing; Canada is choosing, not selling under pressure.

The current government is centrist with an explicit economic-competitiveness mandate.

The Canada Sovereign Wealth Fund framework is operational and available as the federal ownership vehicle.

None of Spain, France, Germany, Turkey, India, or Brazil had all five at decision time.

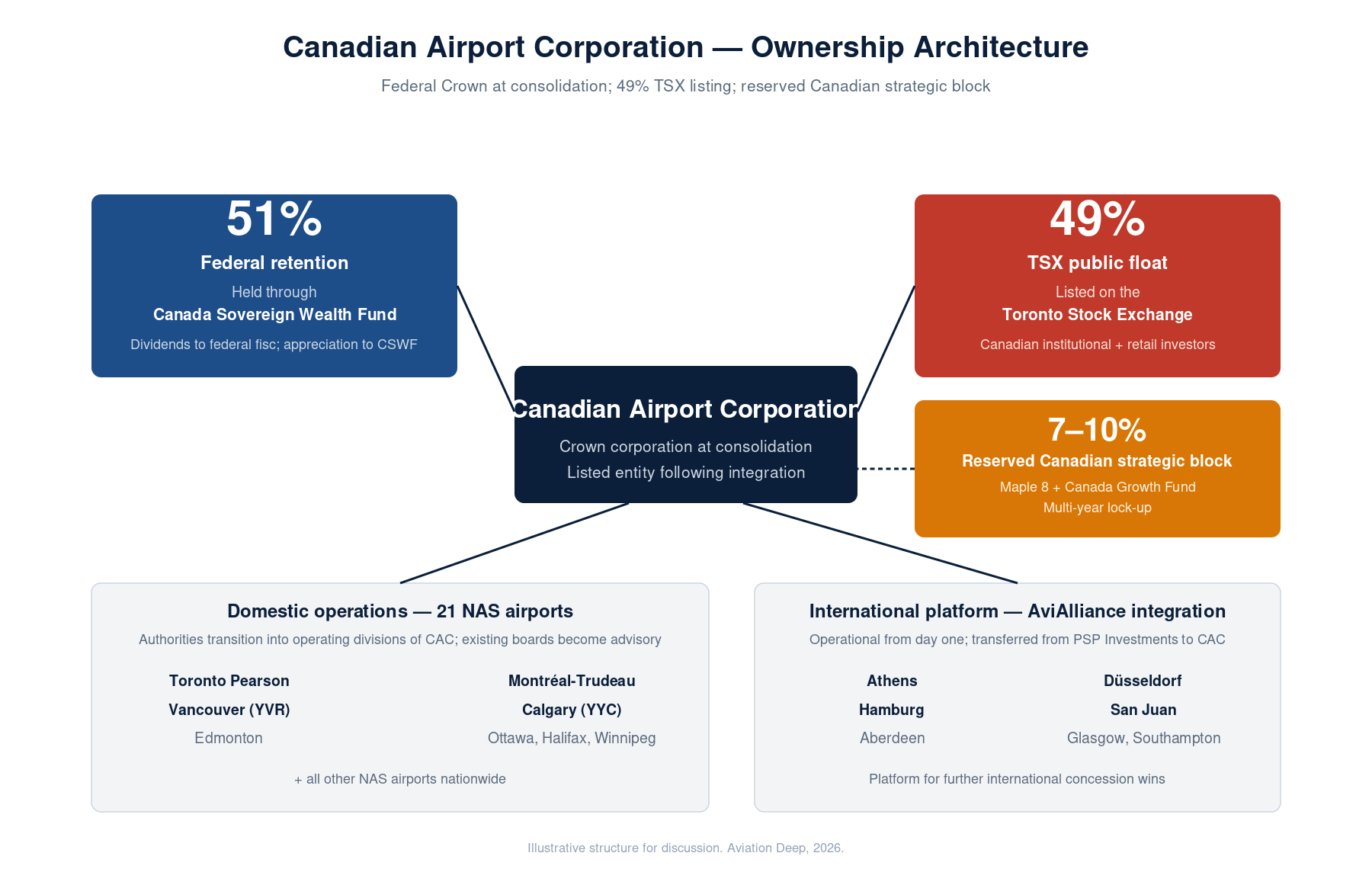

The empirical record and the Canadian conditions converge on one structural design: full consolidation of the twenty-one NAS airports into a Canadian Airport Corporation, with federal retention, a Toronto Stock Exchange listing, and a domestic strategic shareholder block.

The remainder of this piece explains what that structure does, who benefits from it, and what is required to put it in place.

The structure

The recommendation is structural. The twenty-one NAS airport authorities are consolidated into a single Crown corporation: the Canadian Airport Corporation, CAC. The federal government holds 100 percent at consolidation. Once the regulatory framework is operational and the operating systems are integrated, 49 percent of CAC lists on the Toronto Stock Exchange. The federal government retains 51 percent through the Canada Sovereign Wealth Fund. Of the 49 percent floated, a block of 7 to 10 percent is reserved for designated Canadian strategic shareholders — the Maple 8 pension funds and the Canada Growth Fund — under a multi-year lock-up.

Each element of that structure serves the dual-capture argument.

Federal retention through the Canada Sovereign Wealth Fund. The 51 percent stake is held by the Canada Sovereign Wealth Fund, not by Treasury directly. This is the AENA architecture, adapted: in Spain, the 51 percent is held by Enaire, a state holding entity. The vehicle separates the equity stake from the annual fiscal cycle and gives the federal government an instrument designed to manage long-duration infrastructure equity. Dividends on the 51 percent flow to the federal fisc. Capital appreciation accrues to the federal balance sheet through the Sovereign Wealth Fund’s net asset position.

The 49 percent float on the Toronto Stock Exchange. A TSX listing puts equity in CAC into the hands of Canadian institutional and retail investors — pension funds, mutual funds, ETFs holding TSX index exposure, and individual investors through registered accounts. The float is the mechanism by which the second income stream, equity returns, is opened to Canadians beyond the federal Treasury. It also enforces transparency through quarterly reporting, IFRS-audited financials, and the continuous disclosure obligations of a listed entity.

The reserved 7 to 10 percent Canadian strategic shareholder block. This is the design choice that closes the asymmetry established above. Canadian pension funds have, for two decades, captured both income streams as foreign investors. The reserved block — modelled on anchor shareholder arrangements used in major infrastructure IPOs, with the Canadian addition that the block is reserved for Canadian institutional investors — gives the Maple 8 and the Canada Growth Fund a path to hold equity in Canadian airports at home, under a multi-year lock-up that disciplines the investment horizon. Provincial pension entities — CDPQ for Quebec, OMERS for Ontario, BCI for British Columbia, AIMCo for Alberta — fit naturally into this block.

Operating consolidation. The twenty-one airport authorities, including their operating teams, transition into operating divisions of CAC. Toronto Pearson, Montréal-Trudeau, Vancouver, Calgary, and the other authorities each retain their senior operating leadership. Existing board members transition into airport-level advisory boards, preserving the community, business, and municipal representation that the 1992 structure produced. None of the institutional knowledge built over thirty-four years is lost. What changes is that operating margins consolidate at the CAC level rather than being retained and reinvested at twenty-one independent non-profit authorities. This is the mechanic by which the first income stream — operating revenue — becomes available to the federal government and, through the listing, to Canadian equity holders.

The international platform. A consolidated Canadian operator without an international footprint captures only the domestic operating margin. The legislation can authorize CAC to develop international operations in three ways:

Build the capability from scratch, on the AENA Internacional pattern Spain executed over a decade;

Acquire an existing international operator post-IPO, which is capital-intensive and subject to market timing; or

Integrate AviAlliance — the Canadian-owned international operator currently held by PSP Investments, with seven airports across Athens, Düsseldorf, Hamburg, San Juan, Aberdeen, Glasgow, and Southampton — into CAC at consolidation.

The merit of the third path is execution: the platform exists, the operating track record is twenty years long, and the integration can be completed inside the consolidation window. The legislation should authorize the transfer; the timing and consideration are negotiable.