The Joby–Blade Transaction: Wrong on Every Dimension

$125 million for a helicopter brokerage you plan to replace anyway. No aircraft, no pilots, no MRO, and a client base that would have converted regardless. Why?

On August 4, 2025, Joby Aviation announced the acquisition of Blade Air Mobility’s passenger business for up to $125 million. Four arguments anchored the rationale: infrastructure access, a loyal client base, a revenue bridge, and operational expertise. A fifth — one Joby never stated publicly — is more damaging than all four: Joby acquired the business its own aircraft is certified to replace, and in doing so revealed a private view of its certification timeline that diverges from its public one.

Each argument collapses under the factual record.

Part I — What Did Joby

Infrastructure: The Helipads Blade Never Owned

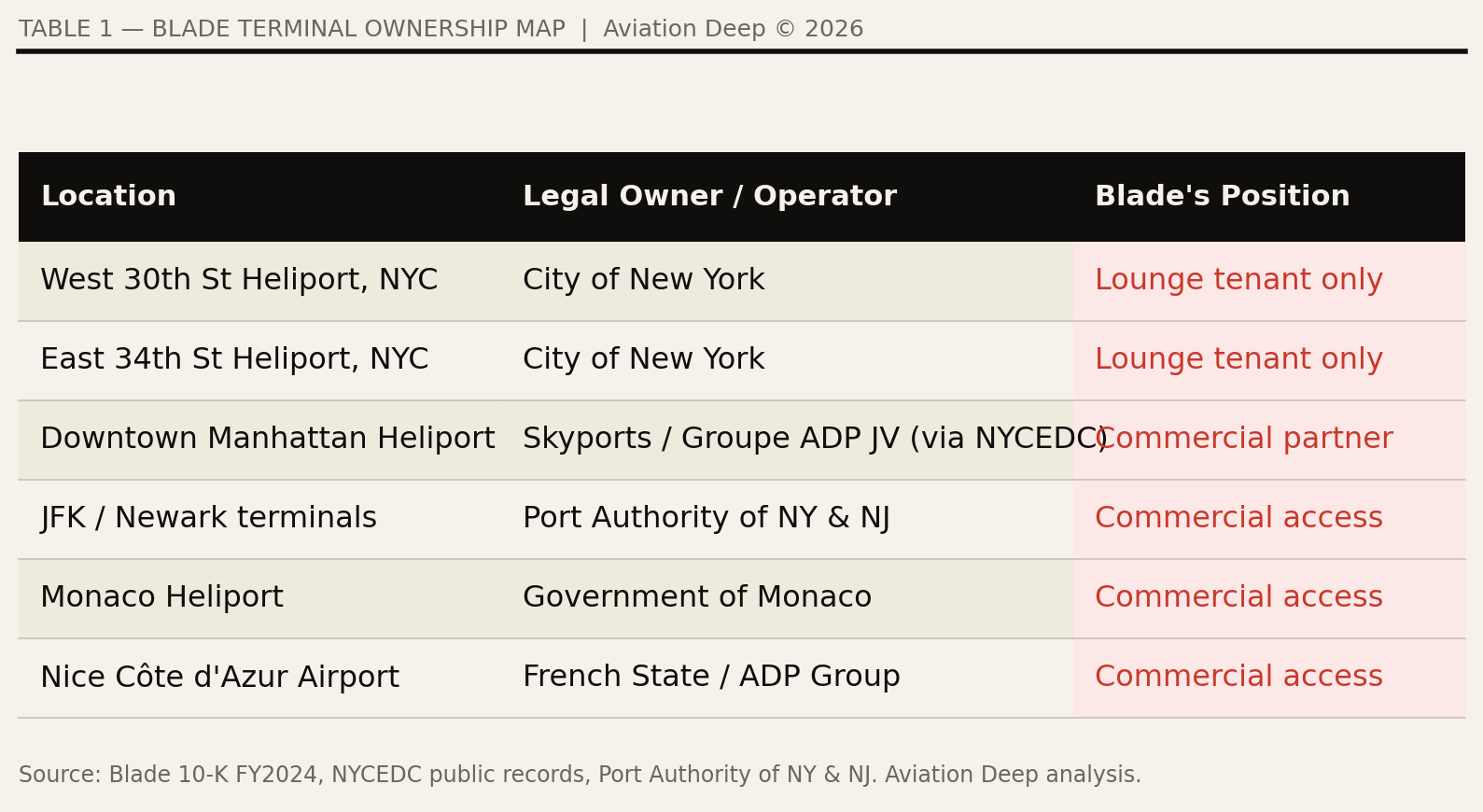

The infrastructure argument rests on a factual error. Blade owns none of the locations it operates from. Every terminal in its network sits on land controlled by a public authority, a state entity, or a third-party operator.

Blade’s position at each location is a commercial tenancy or access agreement — lounge fit-outs and service counters inside facilities it has no ownership stake in, on terms available to any operator willing to negotiate them. The West 30th Street Heliport is controlled by the City of New York. The Downtown Manhattan Heliport is operated by Skyports under a concession from NYCEDC. The Monaco Heliport is owned by the Monegasque government.

Joby needed none of these locations to be owned by Blade to access them. A preferred-partner agreement — guaranteed terminal priority, co-branded passenger experience, route data sharing — would have secured identical operational access for $5–8M over three years with zero liability transferred. Joby paid a ~$110M premium for assets that were never Blade’s to sell.

Client Base: 50,000 Passengers Who Were Coming Anyway

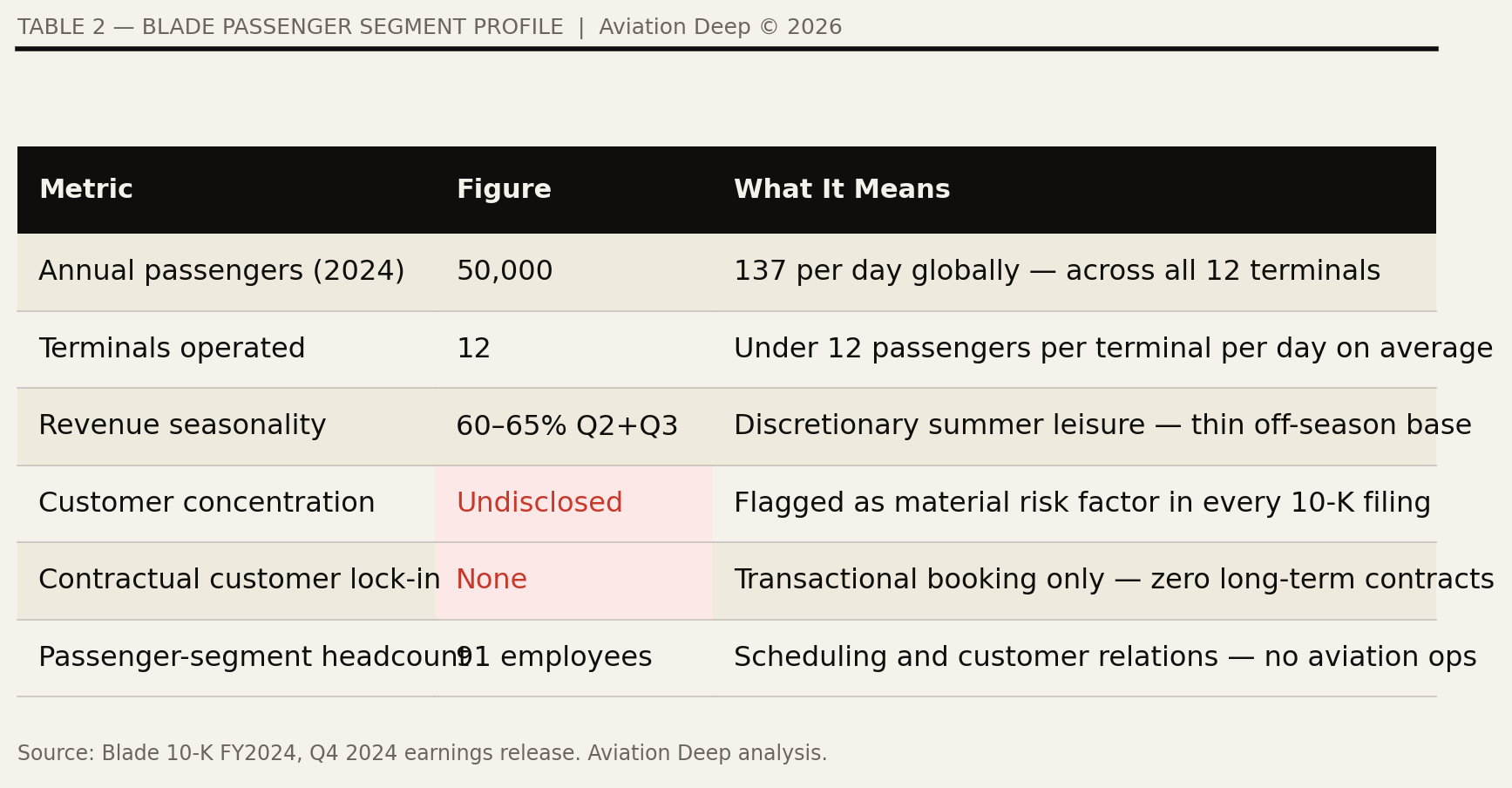

Blade’s SEC filings describe a passenger base far smaller, more concentrated, and more seasonal than the press release framing suggests.

50,000 annual passengers across 12 terminals is 137 per day globally — fewer than 12 per terminal per day on average. 60–65% of revenue concentrates in Q2 and Q3. Blade flagged customer concentration as a material risk in every 10-K filing without disclosing the ratio — an omission that, in SEC disclosure practice, signals the concentration is significant. There are zero long-term customer contracts. Every booking is transactional.

Blade’s premium urban flier is environmentally conscious, time-sensitive, premium-paying, and already habituated to vertical lift — precisely the customer predisposed to adopt eVTOL on product merit. Lower noise, lower operating cost, zero emissions. An aircraft certifiably superior on every relevant dimension to the helicopter attracts the helicopter’s former passengers without requiring a $125M acquisition. A co-branded early-access program and data-sharing agreement would have secured equivalent customer conversion for $2–3M.

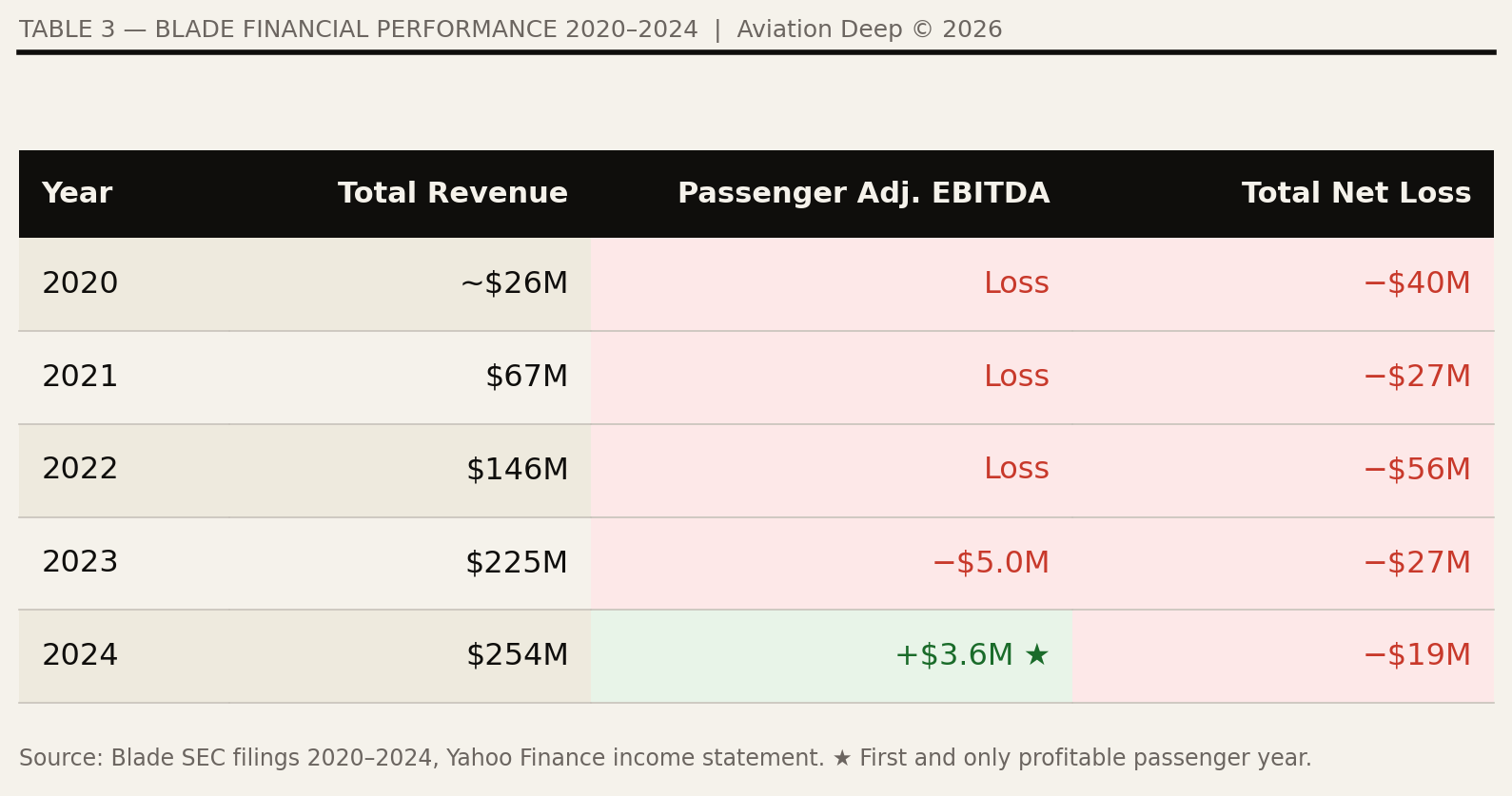

Revenue Bridge: $3.6M Against a $700M Burn

Blade’s five-year financial record makes the arithmetic plain.

The passenger segment lost money in every year of its public life until 2024, when it reached $3.6M in adjusted EBITDA — its first and only profitable year. Joby burns approximately $700M annually in operational cash (H1 2026 guidance: $340–370M, Joby Q4 2025 shareholder letter, February 25, 2026). That $3.6M covers 0.5% of Joby’s annual cash consumption. As a revenue bridge, it is arithmetically irrelevant.

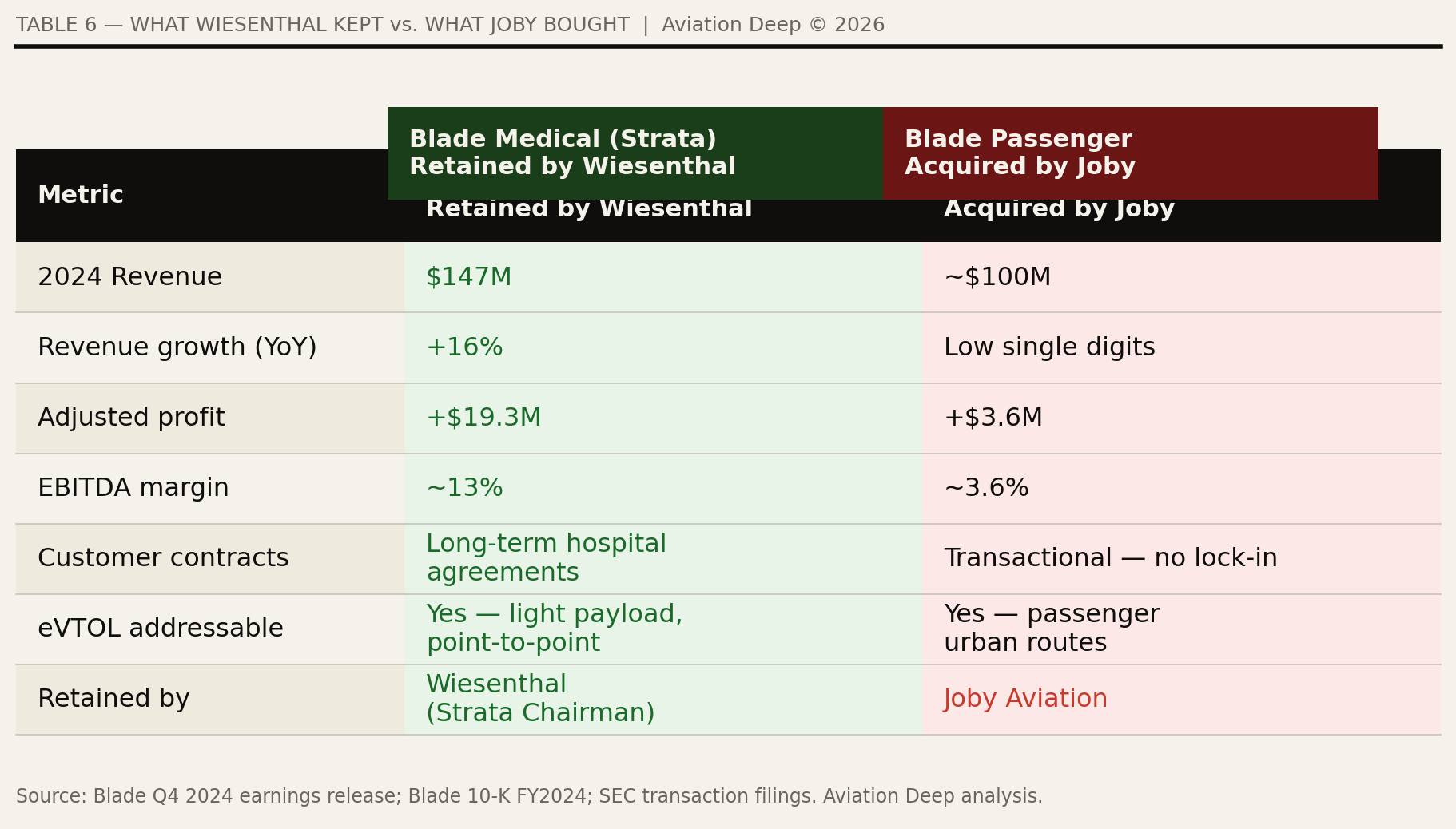

The medical segment — approximately $145M in revenue, 16% year-on-year growth, approximately $17–19M in adjusted EBITDA — generated the overwhelming majority of Blade’s economic value throughout its public history. Wiesenthal retained it as Strata Critical Medical and left Joby with the segment that spent four years losing money and one year breaking even.

At a 30x multiple on $3.6M EBITDA, fair value for the passenger business approximates $108M. The transaction closed at $90–125M — a peak multiple applied to a business at its first and only moment of marginal profitability. Wiesenthal divested the loss-making consumer business at peak narrative valuation, retained the profitable growing medical business, secured a C-suite title at a $15 billion company, and left Joby’s passenger entity with the seasonal discretionary volume that operators will reprice first. There is no public record of him purchasing Joby stock with personal capital despite describing the company in explicitly bullish terms — the transaction terms allowed cash or Joby stock, and the allocation has not been disclosed.

Operational Expertise: A Brokerage That Owns Nothing

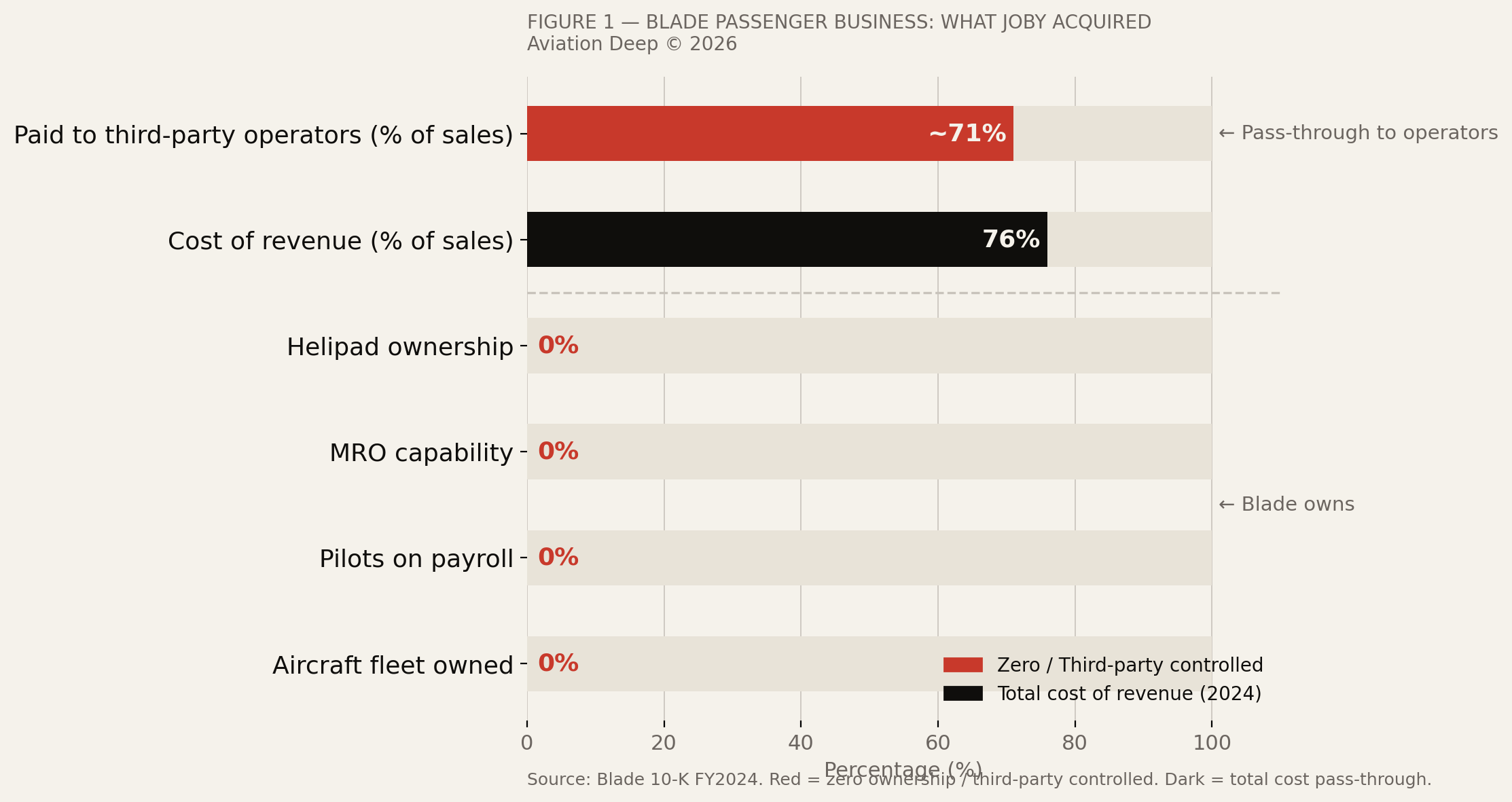

Blade’s own 10-K defines the limits of what Joby acquired:

“Blade leverages an asset-light business model: we neither own nor operate aircraft. Pilots, maintenance, hangar, insurance, and fuel are all costs borne by our network of operators, which provide aircraft flight time to Blade at fixed hourly rates.”

Aircraft owned: zero. Pilots on payroll: zero. MRO capability: zero. Helipad ownership: zero. Cost of revenue ran at 76% of sales in 2024, with approximately 71% flowing directly to operators who own the assets, employ the pilots, perform the maintenance, and bear the insurance. Wiesenthal described the model’s intent in April 2023: “the goal of Blade was to create the entire ecosystem required for EVAs outside of the manufacturing of the aircraft, the operating of the aircraft, and the maintenance of that aircraft.” Blade excluded operational aviation capability by design. Joby acquired 91 passenger-segment employees performing demand scheduling and customer relations.

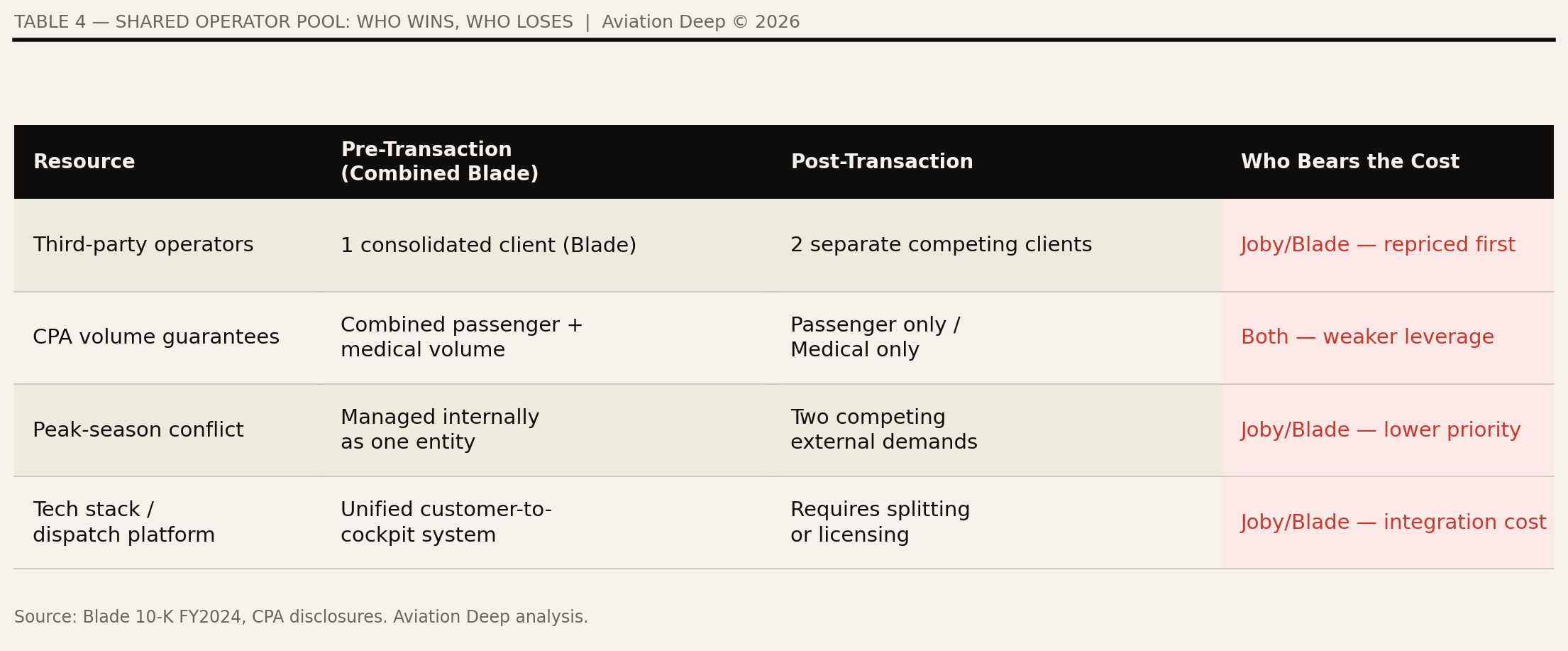

The Shared Operator Pool: One Resource, Two Companies

Blade’s passenger segment — now Joby’s — and Strata Critical Medical draw capacity from the same pool of third-party helicopter and fixed-wing operators. Pre-transaction, combined Blade volume across both segments justified the capacity purchase agreements: fixed hourly rates negotiated on aggregate flying hours across both businesses.

Post-transaction, two separate companies with different ownership, different boards, and different shareholders bid for capacity from the same operator pool.

Strata Critical Medical enters the post-split operator market with approximately $17–19M in adjusted EBITDA, ten dedicated owned aircraft, long-term hospital contracts, and the cash flow to honour volume guarantees. Its medical mission is time-critical — operators prioritise it in dispatch decisions. Joby’s passenger entity enters the same market with seasonal, discretionary consumer demand, zero owned aircraft, and summer-weighted volume that is a fraction of the pre-split combined pool. It is the counterparty operators will reprice first at annual CPA renewal.

Buying What You Intend to Replace

Joby’s S-4/A prospectus, its annual SEC filings, and its earnings calls since 2021 carry the same commercial argument: the S4 replaces the helicopter. Lower noise, lower cost, zero emissions. The helicopter is the incumbent. The S4 is the displacement. That thesis is stated in the certification rationale submitted to the FAA and repeated to institutional investors at every raise.

Joby then paid $125 million to acquire the helicopter business.

The S4 targets Manhattan to JFK, Manhattan to Newark, Nice to Monaco, Hamptons leisure — the exact routes Blade operates. The capital allocated to this acquisition does not accelerate the replacement. It finances the interim operation of the thing being replaced. If the eVTOL product is as compelling as Joby’s filings represent, conversion does not require ownership. Passengers move to superior products. Airlines did not acquire horse-drawn carriage companies to fill their seats.

A company that acquires the business it intends to replace either believes the replacement timeline is longer than it publicly states, or has begun hedging against its own certification thesis. The five-gate certification sequence in Part II places stable US commercial operations in 2029–2030 at the earliest. The acquisition of a helicopter brokerage — a business whose structural life is bounded by Joby’s own certification progress — is the clearest available signal that the private conviction about that timeline is more conservative than the public narrative.

Part II — The Certification Timeline Makes the Timing Indefensible

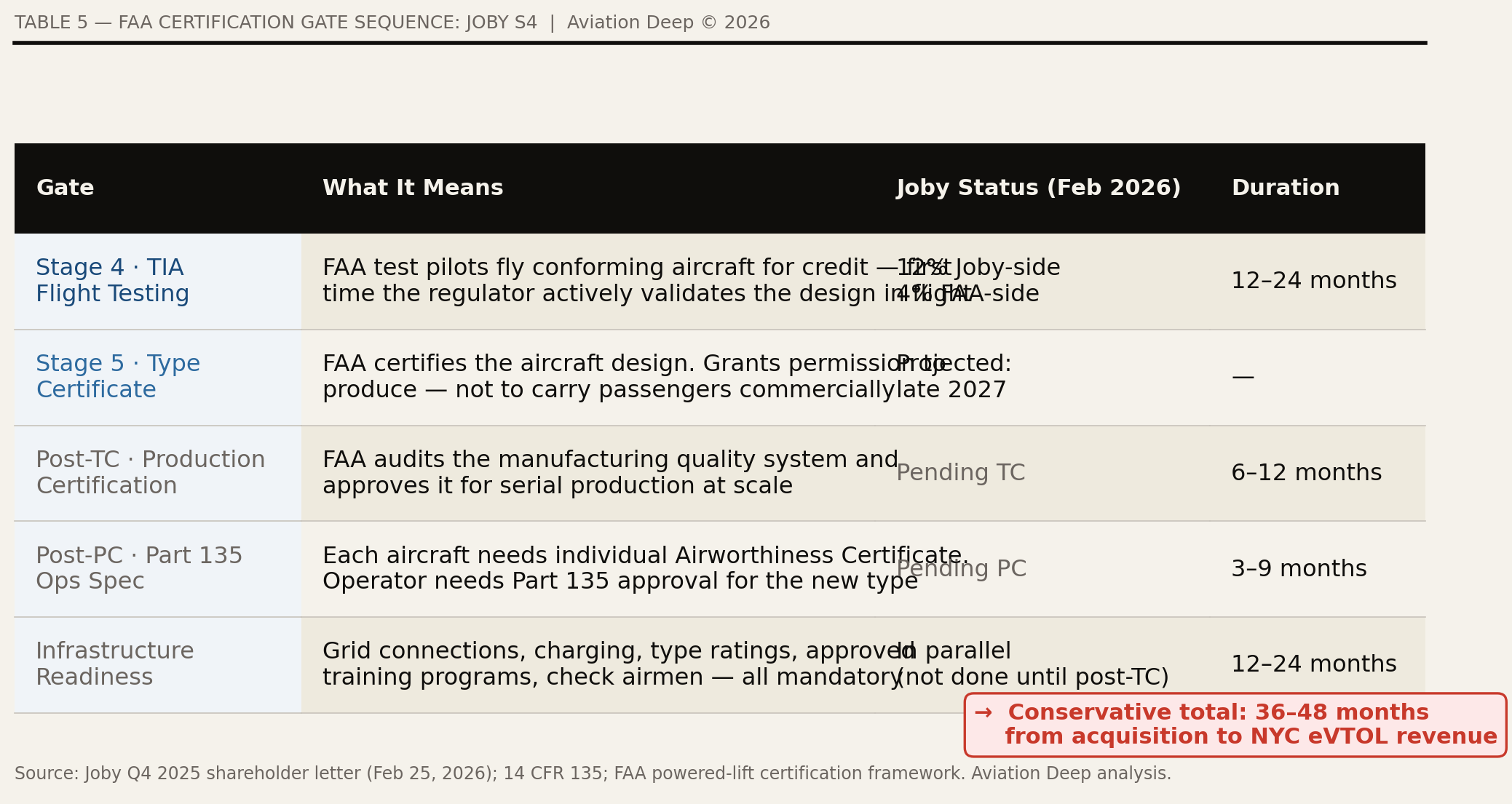

Joby’s press release implied a 12–18 month bridge before the S4 begins replacing Blade’s helicopter fleet. The FAA certification sequence produces a different number. Five sequential gates stand between Joby’s current position and stable commercial eVTOL passenger operations in New York. Each is a regulatory prerequisite for the next. They cannot be run in parallel.

As of February 2026, Joby is at Stage 4 — Type Inspection Authorization flight testing — at 12% Joby-side completion and 4% FAA-side completion (Joby Q4 2025 shareholder letter, February 25, 2026). Based on current stage completion rates and historical gate durations, Type Certificate issuance is projected no earlier than late 2027 — this is an analytical inference from certification stage data, not a direct company disclosure. TC issuance is not commercial permission. It is design certification. Production Certification follows: 6–12 months of FAA auditing the manufacturing quality system. Part 135 Operational Approval follows: individual Airworthiness Certificates per aircraft, Ops Spec amendments, proving runs. Infrastructure readiness — grid connections, charging systems, type ratings, approved training programs — runs in parallel but cannot complete until the aircraft design is certified.

Stable commercial eVTOL operations at Blade’s Manhattan terminals begin in 2029 at the earliest. More probably 2030.

During that 36–48 month window, Joby — a deep technology certification company whose institutional competency is engineering, regulatory navigation, and manufacturing scale-up — operates a consumer helicopter brokerage it has no organizational capability to run. Consumer yield management, third-party operator contract renewal, lounge staffing, seasonal demand planning, and customer complaint resolution compete for management attention during the most capital-intensive phase of the company’s history.

A pre-revenue company burning $700M annually acquired a business generating $3.6M in adjusted EBITDA — then committed management cycles to operating it during Type Inspection Authorization.

Part III — What the Market Already Knew

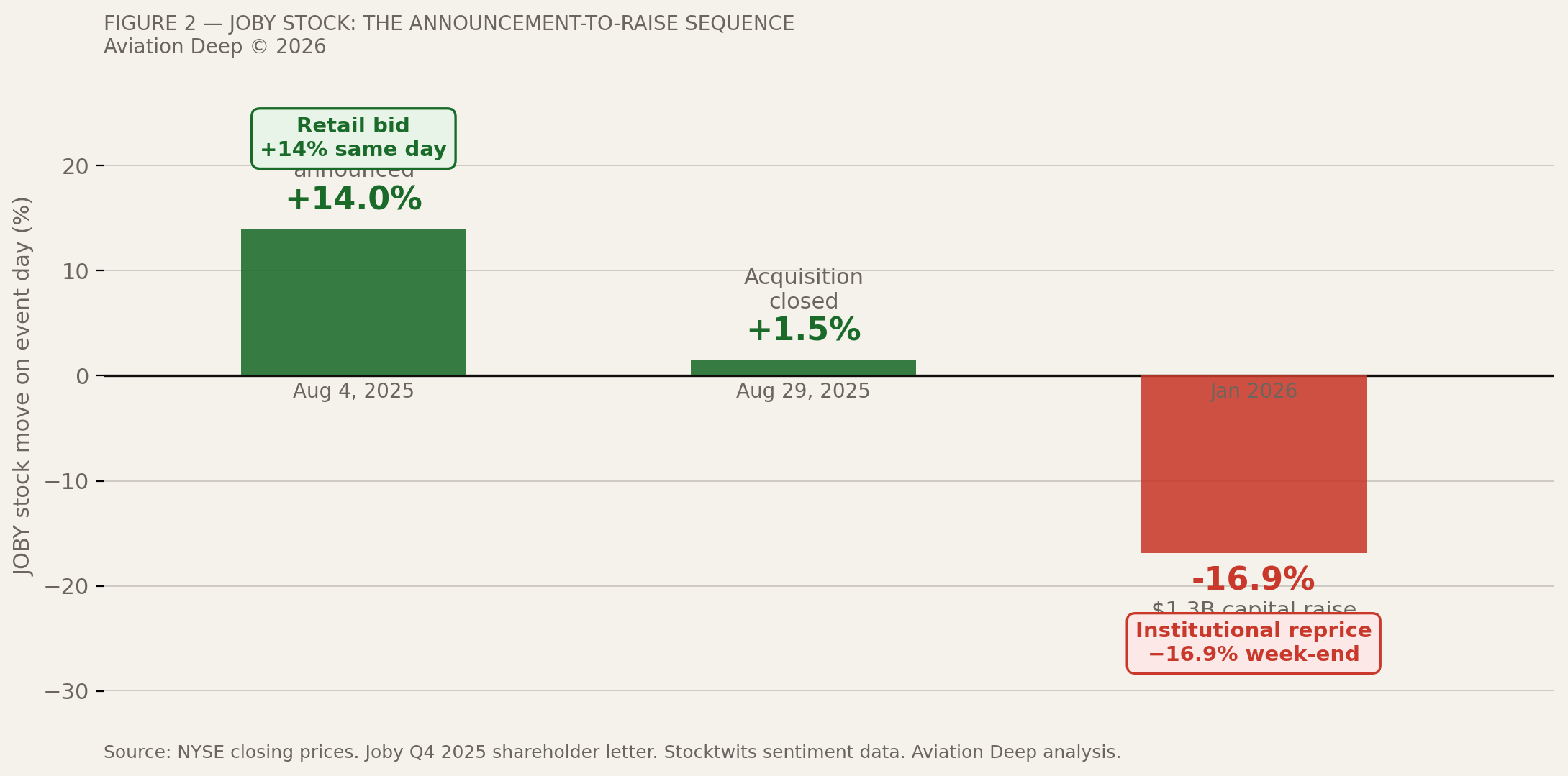

Joby’s announcement history follows a consistent sequence: a headline-generating move, a retail-driven stock spike, and institutional repricing once the financial mechanics become legible to the buyers who read the prospectus. The Blade acquisition ran the same sequence — +14% on announcement day, −16.9% at the January 2026 institutional raise.

Without Blade, Joby enters the January 2026 roadshow as a pre-revenue certification company with a $2.79B accumulated deficit and approximately $700M in annual operational cash use. With Blade, Joby presents $105–115M in 2026 revenue guidance (Joby Q4 2025 8-K, February 25, 2026). On a roadshow deck, helicopter brokerage revenue and eVTOL revenue occupy the same row labeled “Revenue.” The distinction requires reading the footnotes. Institutional buyers participated while simultaneously selling the equity down 16.9%. They provided the capital Joby required. They declined to pay the narrative premium retail had assigned.

The transaction also excluded the one acquisition that would have changed the financial logic: the medical business.

The medical segment is eVTOL-addressable — light payload, short-distance, time-critical missions precisely suited to the S4 profile. It generates approximately $17–19M in adjusted EBITDA against approximately $145M in revenue, with 100% hospital customer retention in 2024. Joby left it on the table. The transaction boundary was not a strategic choice by Joby. It was a divestiture decision by Wiesenthal.